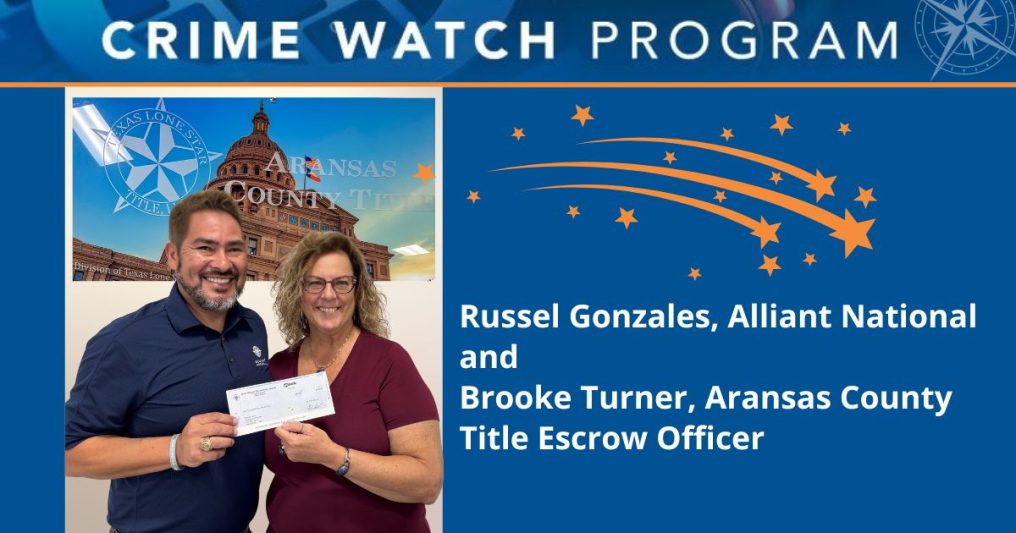

Aransas County Title recently stopped a fraudster cold and became the latest ���dzԹϺ��� Crime Watch recipient By Adam Mohrbacher In the title industry, transaction security can never be secondary. When critical details are overlooked or due diligence is skipped, there can be real consequences for real people. It is for those reasons and more that ���dzԹϺ��� created its …